What the Orderbook Unlocks When It Lives Onchain

The products here span three stages: live on mainnet, in active development, and architectural possibilities not yet built. The article argues for the design, not the ship date.

Executive Summary

Every perp venue has an orderbook. Most run a spot book beside it. Only RISEx runs both as onchain state inside a single EVM, synchronously accessible to each other and to any contract in the same transaction.

This is the difference between a service and a primitive. A service accepts requests and returns results. A primitive is state that other programs can read, write, and compose with atomically.

When a smart contract can read a perp position, buy on the spot book, short the perp, confirm both fills, and act on the result inside one atomic transaction, an entirely different class of product becomes possible: one where the perp is not the destination of a trade but a component of a larger operation, and where the EVM enforces invariants that offchain monitoring cannot.

Six products follow in depth. Each has the same hard requirement: a fill must be a precondition for logic that lives in another program. That is the one tier of atomic composability no async venue can offer.

The Architectural Gap

The comparison is not RISEx versus other DEXes. The comparison is synchronous state access versus asynchronous state access. Hyperliquid and Lighter both run spot and perp books, so the gap is not which markets exist. The gap is whether a smart contract can read one book, act on the other, make each fill a precondition for the next, and revert the whole chain if any leg falls short, all in one transaction.

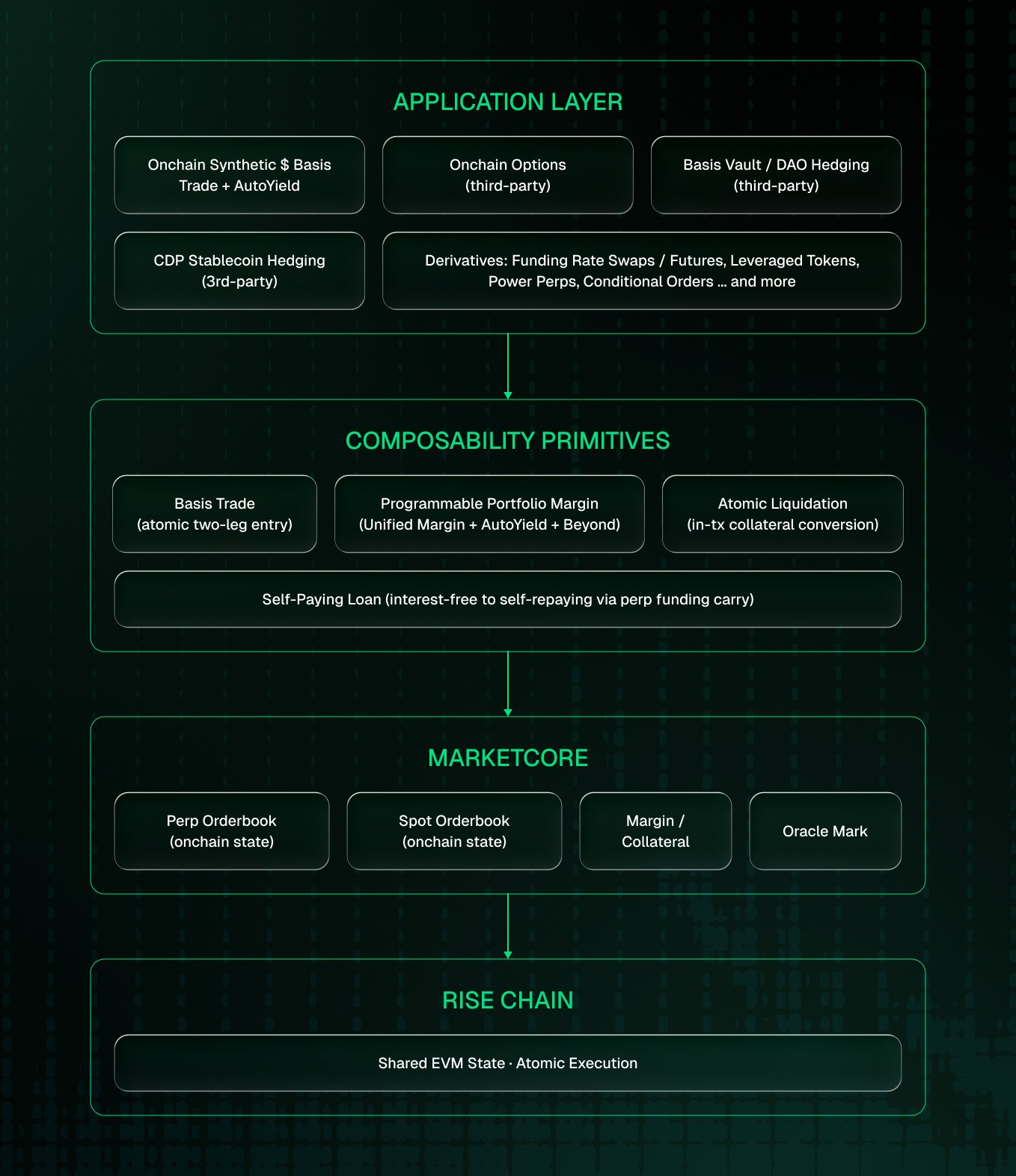

RISE’s matching core is MarketCore: Solidity contracts running inside the EVM, where HyperCore (Hyperliquid) and LighterCore (Lighter) are separated from theirs by an async or proof boundary. For a full architectural comparison, read Composable Books: From High-Performance Trading to Programmable Liquidity. Throughout this article, MarketCore and RISEx refer to the same system and are used interchangeably.

When a smart contract places an order on MarketCore, the fill is a confirmed state change within the same transaction. The contract can check the fill result and branch on it. If the fill does not meet requirements, the transaction reverts, and every prior operation in the transaction reverts with it: the deposit, the token transfer, the collateral lock. The atomicity guarantee extends to the entire chain of composed operations.

What a smart contract can do with RISEx in one transaction covers three categories.

- It can read live protocol state as a precondition: account equity, position size, free margin, best bid/ask, orderbook depth at any price, current mark price.

- It can write state changes that either all commit or all revert: deposit or withdraw collateral, place an order of any type and receive fill confirmation in the same call, execute a spot swap and receive the output amount, move capital between sub-accounts.

- And it can receive hook callbacks from the matching engine into its own contract during execution: fill notification per matched price level, resting order confirmation, maker settlement notification.

- All of this in one EVM transaction, constrained only by block gas limit.

These categories span both books at once. The same transaction can take from the spot book and the perp book, branch on each fill, and revert both if either leg comes up short. The spot leg and the perp leg of a hedge are not two requests to two venues, they are two state writes in one EVM, atomic with each other and with the contract that composed them.

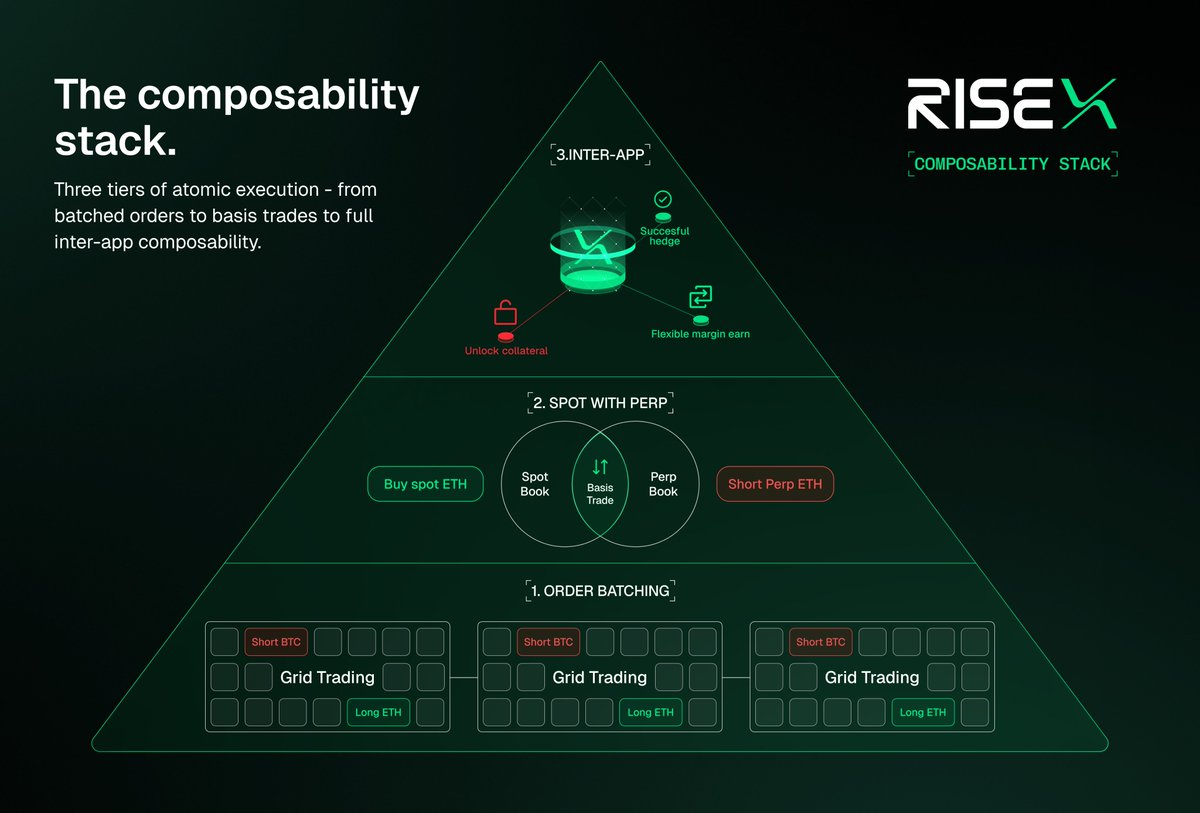

Three Tiers of Atomic Composability

Not all atomic composability is equal. We classify this atomic composability as follows:

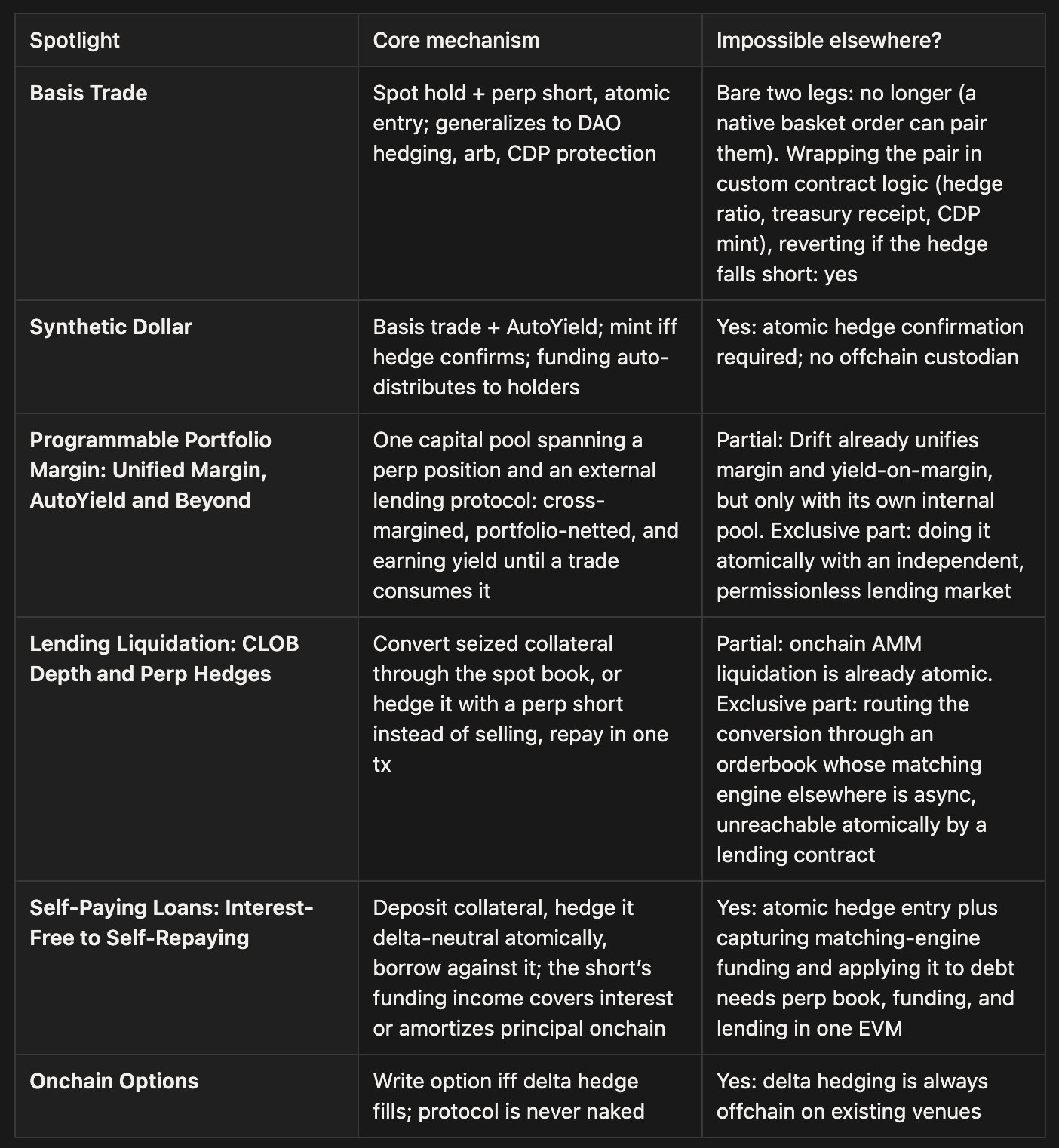

- Tier 1: Order Batching. Order-to-order composability.Multiple orders inside the exchange, filled all-or-nothing, whether in the same market or across markets: a delta-neutral basket of perp longs and shorts, a grid ladder, a sliced entry.

Any venue with a single matching core can offer it, and Lighter ships exactly this as a native atomic order. - Tier 2: Spot with Perp. Cross-product composability.Pair a spot trade with a perp trade in one atomic fill: the bare basis trade, long spot and short the perp together or neither.

Any venue whose spot and perp sit inside the same matching core can support this, which includes Hyperliquid (HyperCore) and Lighter (LighterCore). - Tier 3: Inter-App. Arbitrary logic composability.Make a fill a precondition for logic that lives in a different program: mint a token only if the hedge fills, repay a loan only if the collateral sale clears, keep margin earning in a lending pool until the exact block a trade consumes it.

This needs the matching engine and the other application to share one synchronous execution environment, so the fill is a confirmed state change the other program can read and revert on within the same transaction.

When the matching core is async, the fill is invisible to the application until a later block, in a different execution context.

Every product below is tier 3, or a tier-2 primitive wrapped in tier-3 logic. The basis trade entry is tier 2; a synthetic dollar that mints a token against the confirmed hedge is tier 3. Keep that line in view throughout: the legs are easy, the program built around them is not.

Basis Trade: The Primitive

The basis trade is the simplest complete expression of atomic composability: two orderbook legs that must fill together or not at all. The carry family later in this article builds on it directly; the remaining products share the same underlying capability without running the basis trade itself.

Hold an asset long and simultaneously hold an offsetting short on the perpetual of that asset. The long and the short cancel directional price exposure. The position is delta-neutral: ETH can double or halve, and the net value does not change. What remains after the offset is the basis and the funding rate. When the market is in contango, as it is for the majority of bull market time, short holders earn funding continuously. The trade converts price risk into carry income.

Today

Institutional crypto desks have run basis trades manually for years: buy ETH spot on Coinbase or Binance, short ETH-PERP on OKX or Bybit, harvest the spread. Over the trailing year, accumulated funding ran around 3% on ETH and around 4% on BTC across the major venues, while it spikes far higher in bull runs (ETH funding topped 50% annualized in early 2024) and goes deeply negative on weaker assets in a downturn, as the ZEC row below shows.

Onchain, the bare trade is already run, but a clean fully-onchain version is not. On any venue whose spot and perp share one matching core, such as Hyperliquid or Lighter, a trader can buy spot and short the perp together and farm funding today: pairing the two legs is table stakes. What is missing is a basis trade whose hedge lives in a contract rather than on a CEX, and that other programs can build on. Delta-neutral vaults (Sommelier, some Yearn strategies) automate the pattern but rely on offchain execution or place the two legs in separate transactions. The largest onchain implementation is Ethena, covered in the next section, which scaled the dollar-denominated version but moved the hedging offchain to make it work.

The Limitation: Atomic Legs Are Not Atomic Composability

Pairing two legs is no longer the differentiator: Lighter has shipped a native atomic order that places multiple legs all-or-nothing inside its matching engine. But atomicity stops at the order: it cannot wrap the pair in arbitrary contract logic or revert a DAO’s collateral deposit when the hedge leg fills short.

That hard gap is execution risk whenever the composing logic and the fill are not in the same transaction. A vault that entered a $10M ETH position with the spot leg in block N, then saw the perp leg fail in block N+1 due to a sudden liquidity gap, is holding $10M of unhedged ETH with no guaranteed exit.

The execution risk is not hypothetical: it is the reason existing delta-neutral onchain vaults either restrict position sizes aggressively or maintain large reserve buffers to absorb the possibility of stranded single-leg positions.

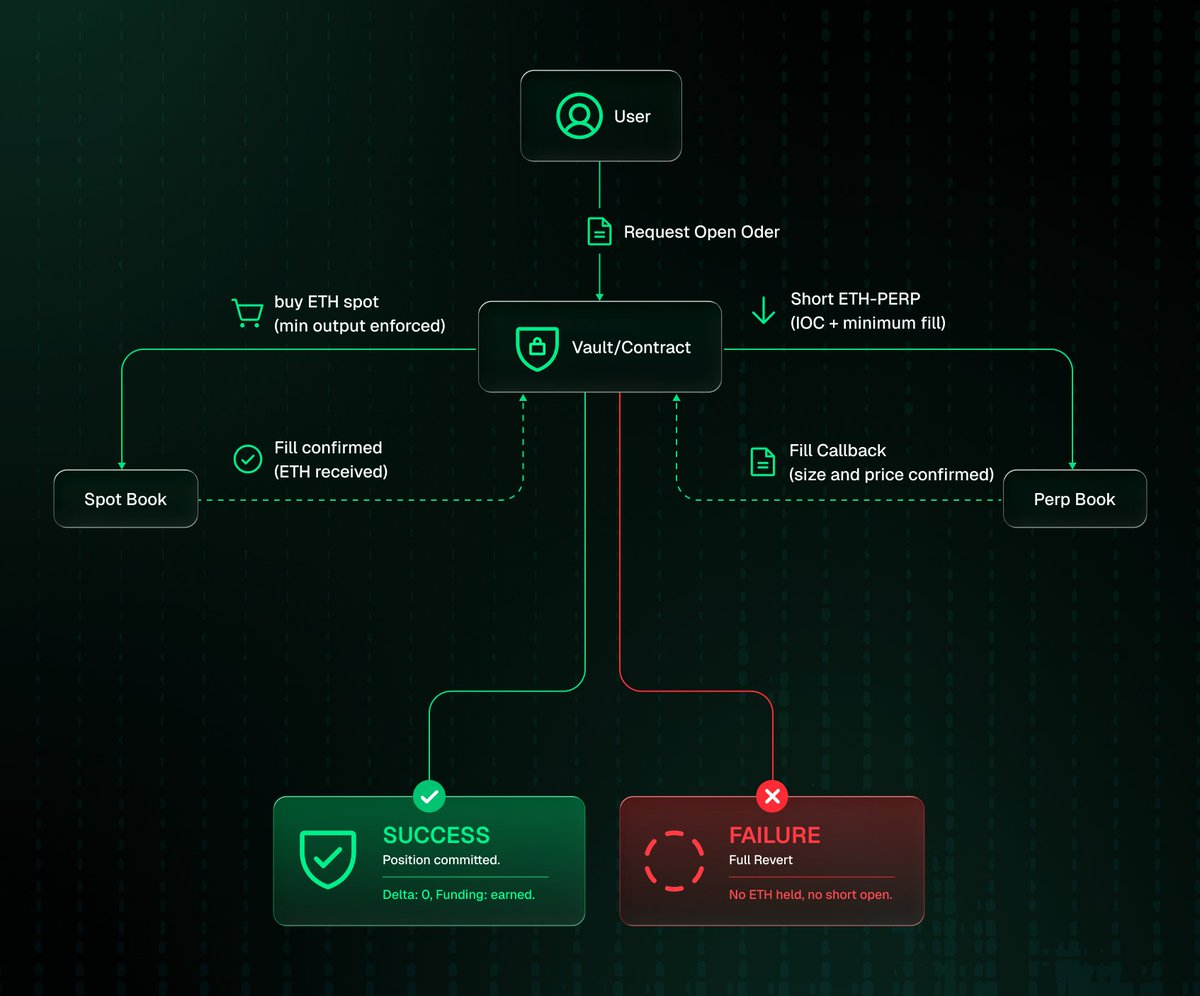

With Atomic Composability

Both legs are placed in a single transaction with minimum fill requirements on each. The spot buy executes, then the perp short executes against the live orderbook, then the fill callback confirms the matched size. If the perp short fills below the minimum, because the book thinned between the keeper’s observation and the block’s execution, the entire transaction reverts, taking the spot buy with it. No stranded position, no reserve buffer needed: the vault only enters when it can lock both legs at acceptable prices simultaneously.

The same atomic entry applies beyond the narrow basis trade.

- An arbitrageur capturing a spot-perp premium buys spot and shorts the perp in one shot, or reverts: no position opened against a spread that no longer exists.

- A DAO hedging its treasury opens a perp short in the same transaction that ETH enters.

- A stablecoin protocol minting against new collateral hedges it in the same call, so the protocol never holds unhedged ETH even transiently.

Spot or collateral long, perp short, atomic entry: the context changes, the structure doesn’t.

Risks

RISEx makes the trade trustless and atomic, not risk-free. It removes the execution and custody risks; the market risks of funding and basis remain (e.g, negative funding, short-leg margin and liquidation, basis divergence), and every product built on the basis trade carries them.

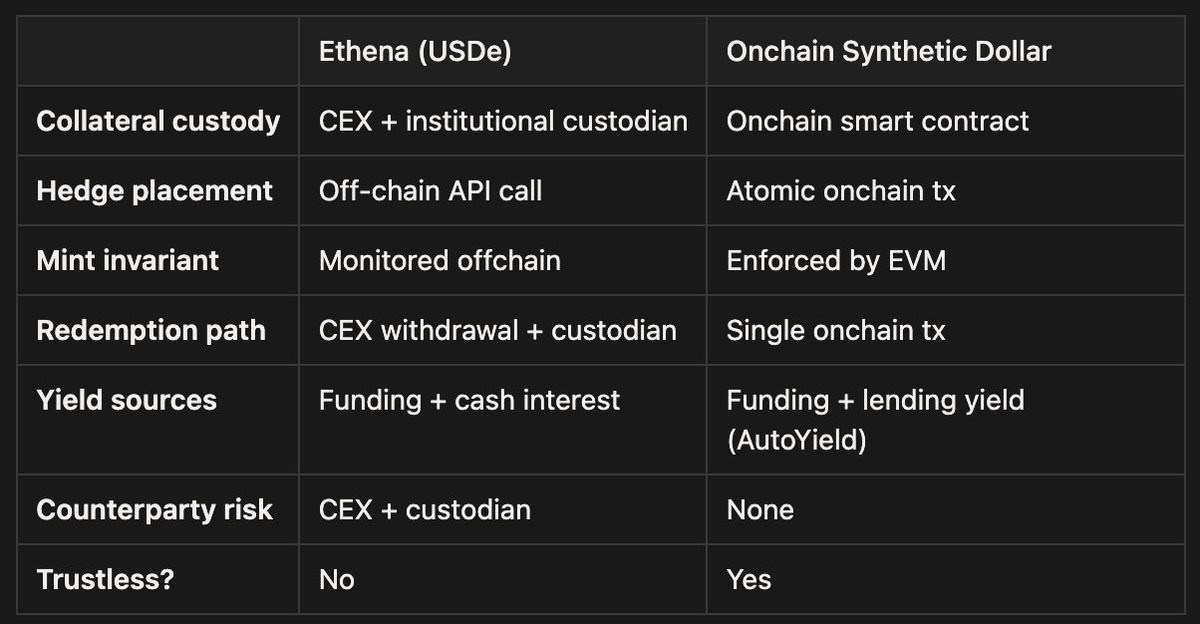

The Onchain Synthetic Dollar

The synthetic dollar extends the basis trade into a fully-featured monetary product: a token that is stable in dollar terms, earns yield from two sources simultaneously, and is entirely trustless.

Today

Ethena’s USDe is the canonical implementation: the delta-neutral basis trade applied to a dollar token. USDe grew into the third-largest dollar-denominated stablecoin, behind only USDT and USDC, with supply peaking above $12B in 2025 before contracting to around $4.8B by mid-2026.

The mechanism is sound. The trust model is not. Ethena’s short positions sit on Binance, OKX, Bybit, and other CEXes, managed by institutional custodians Copper and Ceffu. Ethena’s own risk documentation states this plainly. The FTX collapse is the template: the same off-exchange custody structure made those users vulnerable.

The trust surface: Ethena must trust (a) that Copper/Ceffu hold the collateral honestly, (b) that the CEX does not halt withdrawals, and (c) that the hedge can be closed when redemptions require it. Any one failure breaks the peg.

Beyond the trust model, Ethena faces a structural limitation on yield. The yield has two components: funding income from the short position, and interest on the cash collateral held by the custodian. There is no mechanism to earn additional yield from the perp margin itself while the position is open.

With Atomic Composability

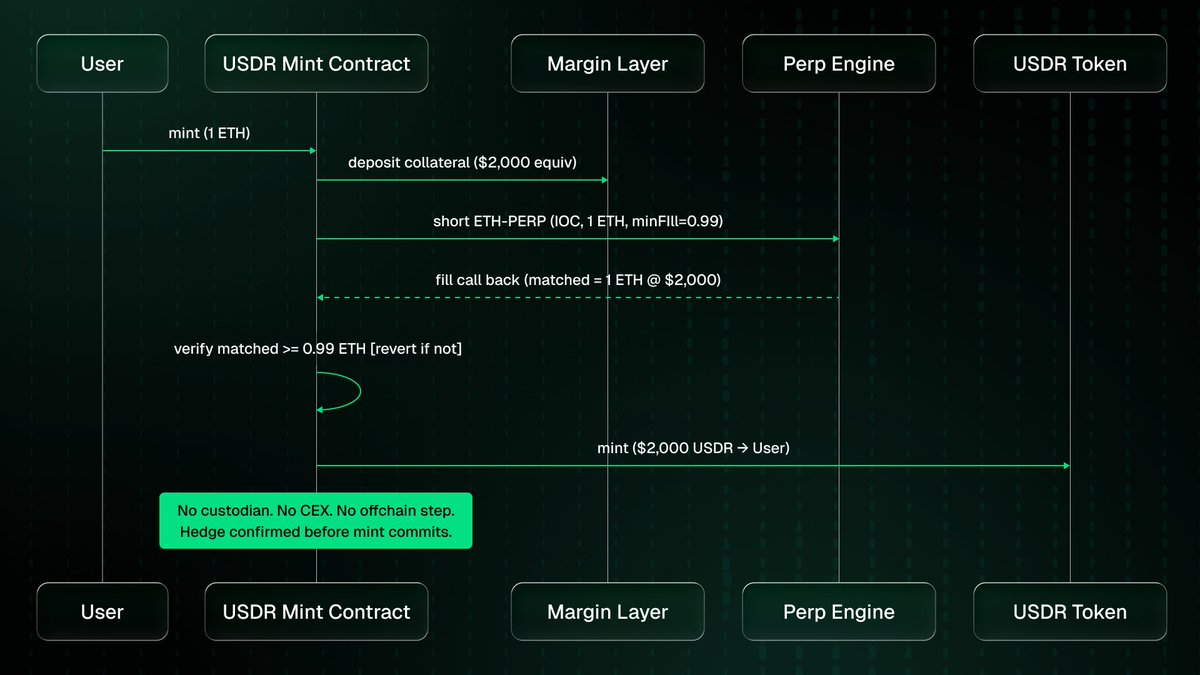

On RISEx, the mint invariant is enforced at the transaction layer. A user deposits ETH. In a single atomic transaction: the contract accepts the collateral, places a short ETH-PERP, receives the fill callback with confirmed size and price, verifies the fill, and only then mints a synthetic dollar token (e.g., let’s say USDR) proportional to ETH deposited times the mark price. If the fill is insufficient, the entire transaction reverts: no collateral taken, no dollar minted. The invariant holds by construction: every USDR in circulation is backed by a confirmed hedge.

Redemption works the same way: burn USDR, close the short, return ETH, all in a single transaction with no withdrawal queue, no custodian to route through, no CEX that can block the exit.

The yield layer is compounded. The short position earns funding payments whenever the perp trades above spot. Simultaneously, the idle USDC margin deposited against the short is deployed into a lending protocol via the AutoYield mechanism described in the next section, earning lending yield on top of the funding income.

The fully onchain synthetic dollar is not a better Ethena. It is a different category of product: trustless, permissionless, and auditable at any block.

Programmable Portfolio Margin: Unified Margin, AutoYield and Beyond

The same dollar of capital should be able to do multiple jobs at once: back a perp position, satisfy the collateral requirement of a loan, and earn yield while it waits.

Today: Already Real, But Limited

None of this is hypothetical, and none of it is unique to RISEx. The pattern is old in TradFi (portfolio margining at prime brokers); CeFi crossed it in 2021: Binance portfolio margin nets spot, margin, futures, and options into a single requirement. No yield: the margin sits idle between trades.

Lighter offers unified spot-perp netting, similar to Binance, but stops at netting. Hyperliquid and Drift go further by adding yield on top. Hyperliquid pairs spot-perp netting with an integrated lending market on testnet, while Drift delivers the most complete version on Solana perps, spot, and lending all in one cross-margin account, with collateral earning yield while backing positions, settled atomically.

However, all of them only unify what they control internally. The lending pool, rates, assets, and risk parameters belong to the exchange itself. Traders can’t access the best yields across DeFi, and the same capital can’t simultaneously serve as collateral in an external lending protocol while acting as margin for perps.

In short, the unification hits the boundary of each protocol. Hyperliquid, for example, must choose between thin but atomic lending inside HyperCore, or rich but asynchronous lending on HyperEVM.

The Requirement: Atomic Composability Between Protocols

A protocol acting on that stale reading accumulates bad debt through stale data, not malice. The multi-protocol health check is only trustworthy if it is atomic.

Drift solves this by collapsing both protocols into one: if the lender and the perp engine are the same program, their state is trivially coherent. The price is that the lender has to be the exchange. The unsolved version is the same coherence across two protocols that nobody owns jointly.

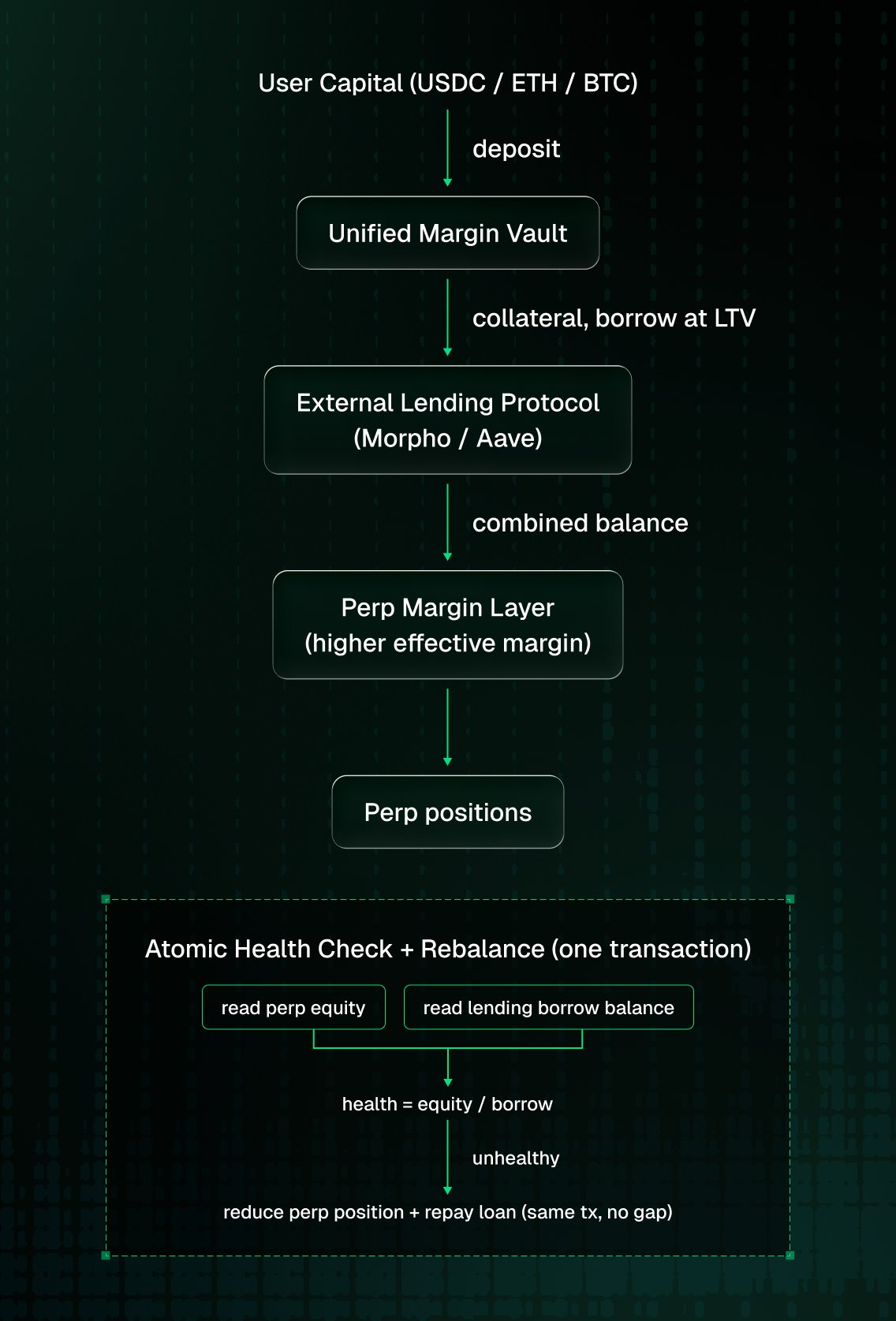

Programmable Portfolio Margin

Margin State is EVM Storage. The matching engine runs in the same EVM as every other contract. An external contract can read live account equity, position delta, and free margin as a precondition, then write to both the perp book and an external lending protocol in the same transaction, with the whole chain reverting if any step fails. The netting is not internal bookkeeping the exchange exposes through an API, it is state any program can act on. The exchange does not have to be the bank: margin can compose with, and earn yield from, any external lending market, Morpho, Aave, Euler, chosen for the best rate, and a new lender can plug in permissionlessly without the exchange listing it.

Collateral is not limited to USDC. ETH, BTC, and any other asset accepted by RISEx can serve as margin simultaneously, each deposited into its own external lending market and earning yield there while collectively backing the same perp book.

Two concrete applications of programmable portfolio margin:

Unified Margin. A vault holds the user’s capital and intermediates both protocols at once. It deposits USDC into an external lending pool as collateral, borrows against it (say 80% LTV), and posts the combined balance as perp margin, so $10,000 of capital backs $18,000 in effective perp margin (1.8x at 80% LTV) while the lending collateral requirement is satisfied from the same pool.

The joint health factor, perp equity over outstanding loan, is read from both protocols in one transaction. When it drops, the vault rebalances atomically: read free margin, place a reduce-only order to partially close the position, withdraw the freed collateral, repay the loan, four steps in one transaction. The position is never reduced without the proceeds immediately repaying the loan. No state where the position is closed but the debt is outstanding, no capital idle between the two.

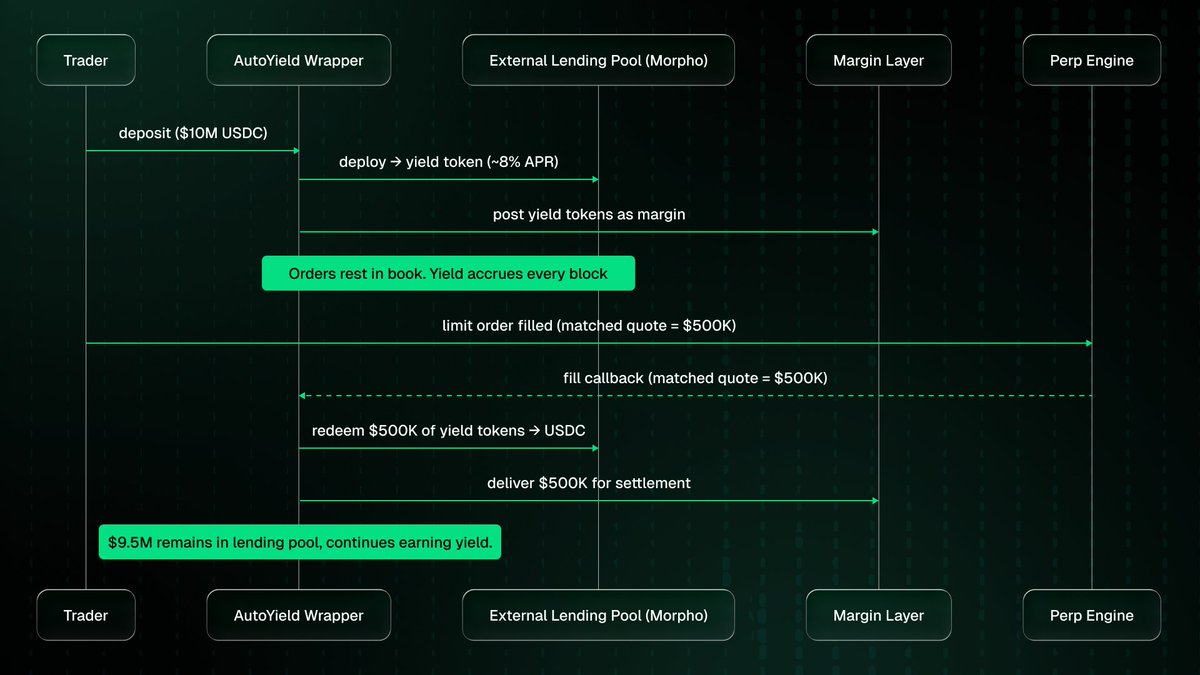

AutoYield. The margin earns in an external lending market until the exact instant a trade consumes it. A yield-forwarding wrapper deploys idle margin into the lending pool, posts the yield-bearing tokens as margin, and on the callback redeems exactly the matched amount for settlement, all in the same transaction.

Only the consumed portion leaves the pool; the rest keeps earning. For a market maker whose orders fill 20% of the time, 80% of margin earns continuously: on $10M at 8% APR, roughly $640,000 a year recovered from capital that was idle.

Programmable portfolio margin extends to anything that requires margin. Unified margin and AutoYield are two applications. Any protocol that holds, manages, or acts on margin can compose with the same open state: read account equity, write to the perp book, receive fill callbacks, in one atomic transaction. Margin state is open EVM storage, and no permission from the exchange is required to build against it.

Lending Liquidation: CLOB Depth and Perp Hedges

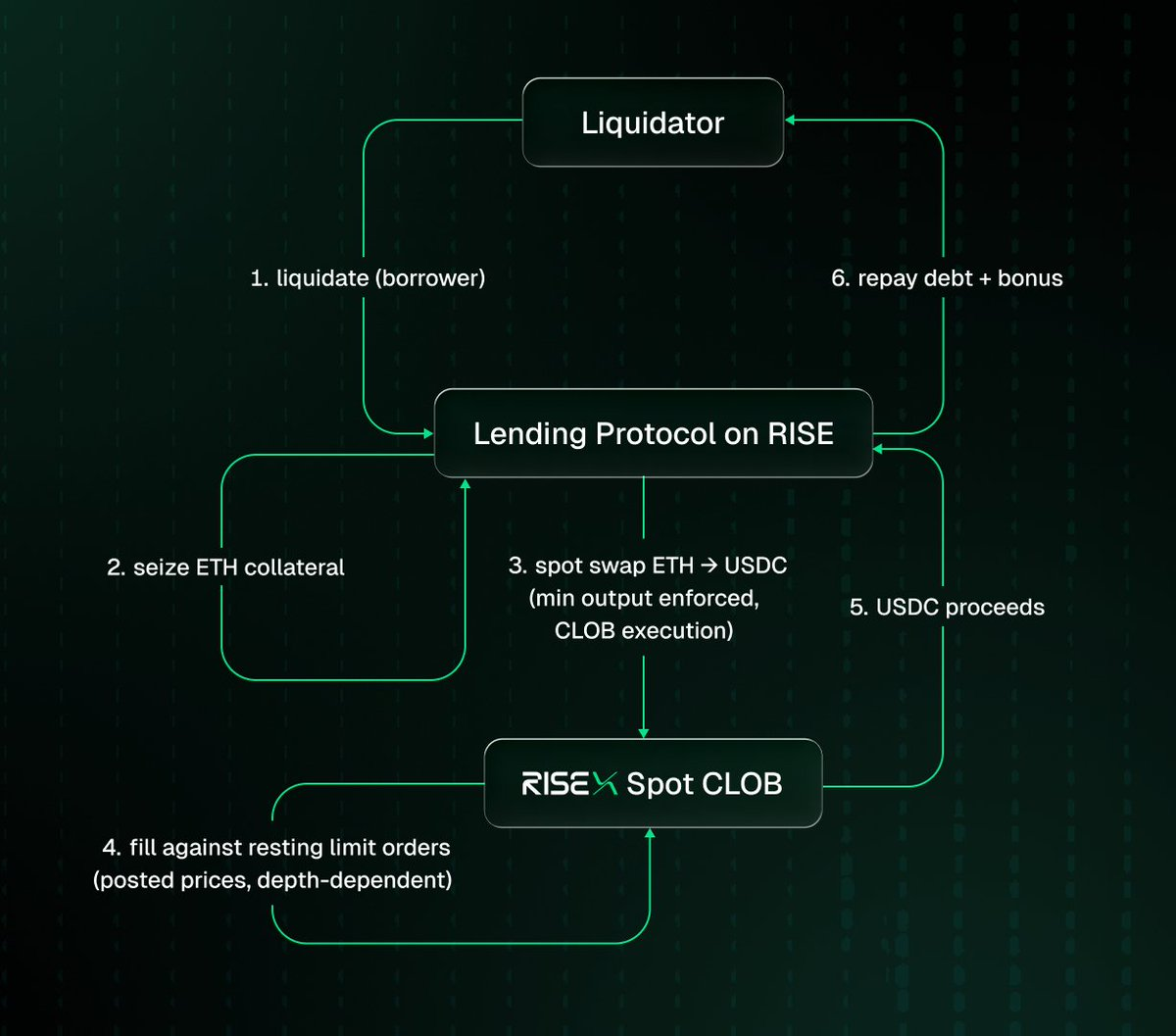

Liquidation is the stress test of any lending protocol: seized collateral must be converted to repay the loan, and solvency rides on that conversion executing cleanly. Today the only atomic conversion route is an AMM. A spot CLOB and a perp hedge change that, but only if the states are shared.

The Constraint

The dominant pattern flash-borrows USDC, calls liquidate() to seize collateral, swaps it through Uniswap or Curve, and repays the loan, all in one transaction. Aave V3 sets a configurable liquidation bonus per collateral asset, typically 5-10%, which is the market price for conversion risk: slippage on the collateral sale, plus gas and latency to win the liquidation race.

When conversion liquidity dries up, the mechanism fails. On Black Thursday (March 2020), gas congestion prevented keepers from processing auctions fast enough: $8.32M of ETH cleared for 0 DAI, leaving Maker with bad debt covered by emergency MKR issuance.

This is a liquidity problem, not an atomicity one. Flash-loan liquidations on Ethereum are already atomic. The reason they route through AMMs is structural: the AMM is the only conversion venue a liquidation contract can reach inside the transaction. CLOB liquidity, often deeper, sits on async matching engines a lending contract cannot touch. The protocol falls back to AMMs regardless of which venue has better depth.

With Atomic Composability

On RISEx, the spot CLOB joins the AMM as an atomically reachable conversion venue. A liquidation contract can seize collateral, swap it against resting limit orders with a minimum-output floor, repay the loan, and pay the bonus, all in one transaction that reverts if the fill misses the floor. The win is optionality: route to whichever venue has better depth for the asset and size.

Hedge Instead of Sell. Dumping large collateral on any spot venue (AMM or CLOB) moves price against the protocol. The perp book offers a second route: atomically open a short perp of equivalent notional against the collateral. The combined position is delta-neutral: further price drops are offset by gains on the short, the loan stays covered, and the collateral can be unwound gradually rather than force-sold.

The tradeoff is explicit: instantaneous price-impact loss vs. a managed funding carry. It also requires perp book depth sufficient to absorb the notional; on a thin book, the partial fill reverts and the protocol falls back to the spot sale. It exists only because the perp book and the liquidation check share the same synchronous EVM. This is the basis trade applied to lending collateral.

Self-Paying Loans: Interest-Free to Self-Repaying

The idea is simple: a loan that costs nothing, or one whose debt erases itself. A self-paying loan can mean either.

- In the weaker form, the collateral’s yield covers the interest charge: the borrower carries the loan for free without sending a payment.

- In the stronger form, yield exceeds the interest rate and the surplus amortizes principal: the balance falls without the borrower touching it.

The DeFi precedent is Alchemix, which deploys deposited collateral into lending or staking yield and applies that yield to the loan. The yield engine there is modest: a few percent a year from stablecoin lending or staking.

Funding income on a delta-neutral basis position is a different, often far larger engine. A short perp held against spot collects funding whenever the perp trades above index, which is most of an uptrend, at annualized rates that run modestly positive in calm periods and spike well above 50% at bull-run peaks.

The Gap

Self-repaying loans exist. But the yield is whatever a lending market or staking pays, and the collateral keeps full price exposure, so a volatile-collateral version still carries liquidation risk.

Basis funding exists. Ethena has harvested perp funding at scale for years. But its hedge sits on CEXes via custodians, so the funding accrues in accounts no onchain lender can read or draw against. On an async venue the funding settles inside the matching core, invisible to a lending contract on the EVM side. The carry is real, it is just not composable with debt.

Closing the Gap

The loan and the hedge open in one transaction, and the funding the hedge earns is applied to the debt onchain.

This shares Ethena’s engine, a delta-neutral basis position earning funding, but not its product. Ethena and the synthetic dollar above mint a dollar token for the world and pay the funding to its holders. Here nothing is minted: the funding pays down one borrower’s own loan, and the borrower reclaims the collateral when the debt clears.

Worked Examples

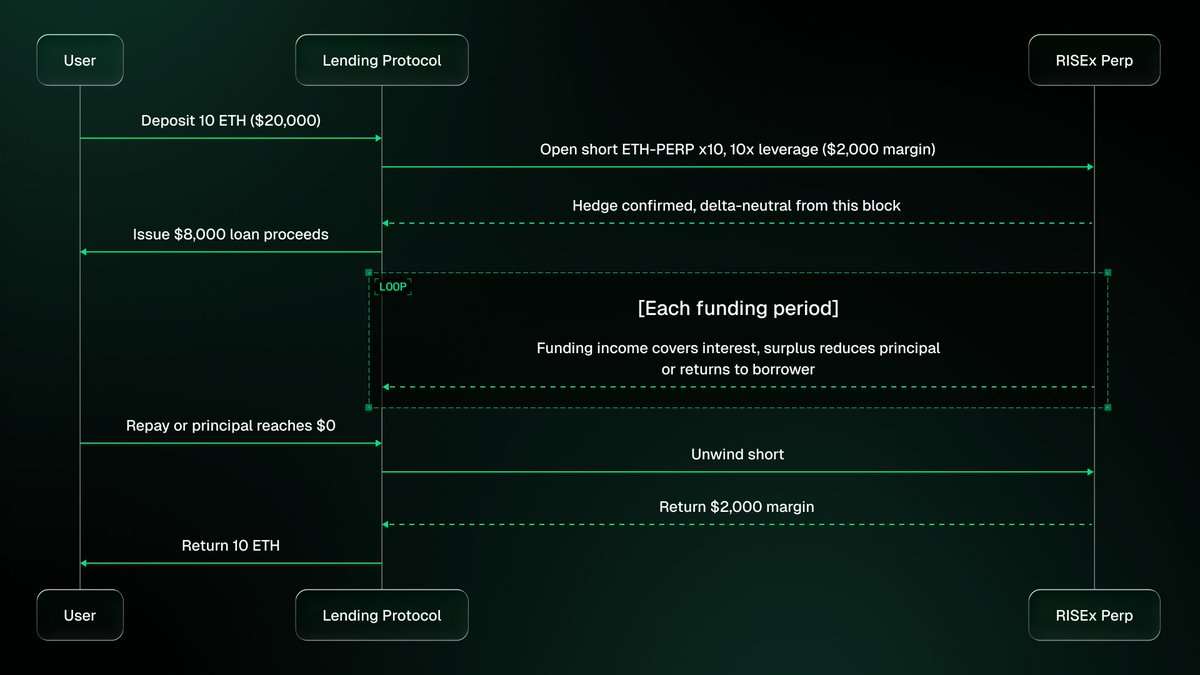

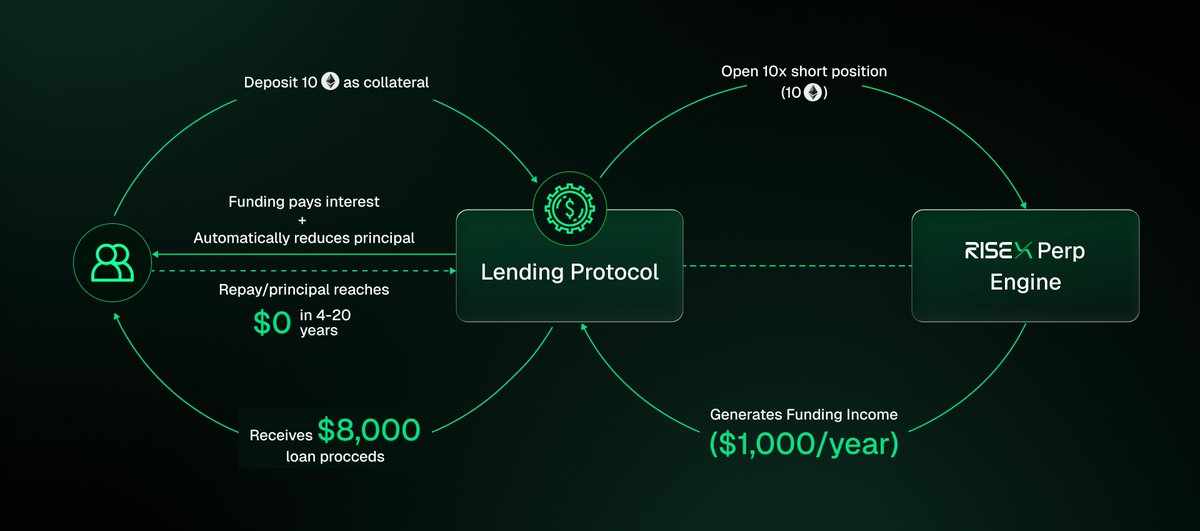

Both modes share the same setup. Deposit 10 ETH at $2,000 ($20,000 collateral), borrow $10,000 (50% LTV). Use $2,000 of that as margin to open a 10 ETH short position at 10x leverage ($20,000 notional); the remaining $8,000 is the borrower’s proceeds. Funding APY on the short = 5%; borrowing rate = 5%.

Funding income: 5% × $20,000 = $1,000/yr. Interest cost: 5% × $10,000 = $500/yr. Net surplus: $500/yr.

Interest-Free Mode. The $500/yr interest is fully covered by the funding income. The remaining $500 surplus is returned to the borrower. The loan carries indefinitely at zero out-of-pocket cost; principal stays flat at $10,000.

Self-Repaying Mode. The full $1,000 funding income is applied: $500 covers interest, the remaining $500 reduces principal each year. The $10,000 balance clears in 20 years, and the borrower never sends a payment. At higher funding rates the timeline compresses sharply: at 15% annualized funding, net surplus rises to $2,500/yr and the same loan clears in 4 years.

Because the collateral carries no price exposure, an ETH crash does not liquidate it: a loan whose health barely moves with the market.

The caveat is funding itself. When the perp trades below index, in backwardation, the short pays funding instead of earning it, and the debt grows rather than shrinks. Positive funding has been the bull-market norm, but it is not a guarantee, and two things can pressure this loan.

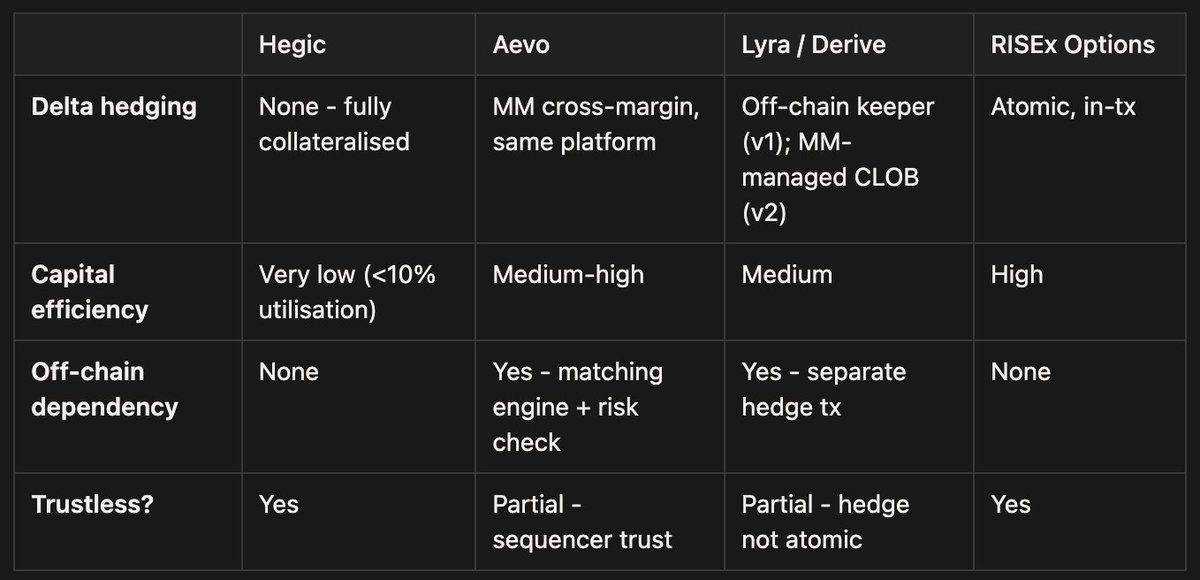

Onchain Options with Live Delta Hedging

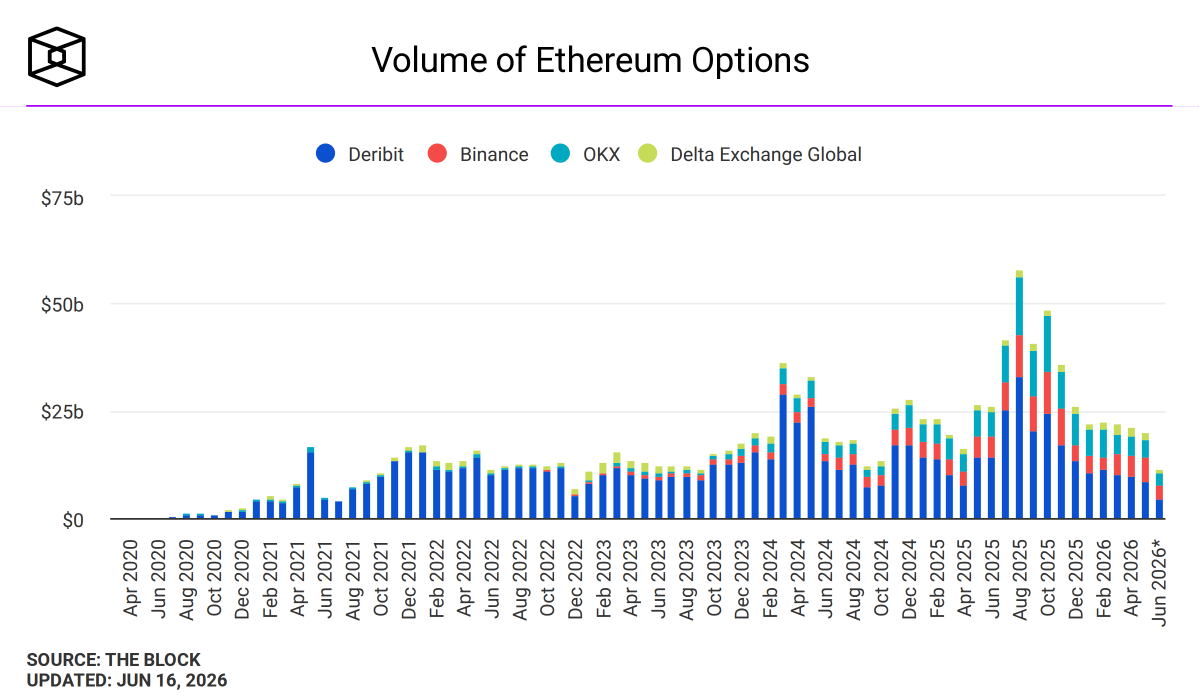

Options on crypto assets are a multi-hundred-billion-dollar market. Deribit alone processed $33 billion in ETH options volume in August 2025, dominating the market across all venues combined. The DEX equivalent remains a fraction of that, for a structural reason.

Existing Approaches

Options market making requires continuously maintained delta hedging. A market maker writing a call option on ETH is synthetically short volatility and long the option’s delta: as ETH price rises toward the strike, the call becomes worth more, and the market maker owes that gain to the buyer. The offset is a long ETH-PERP position equal to the option’s current delta. As price moves and delta changes, the hedge is adjusted. Without it, the market maker has a naked book.

Fully Collateralised Options (Hegic). Option writers post the full maximum payout as collateral upfront.

- No delta hedging is needed because the worst case is already funded.

- The tradeoff is severe capital inefficiency: a market maker writing a $2,100 strike ETH put with ETH at $2,200 must post $2,100 per option (the maximum payout if ETH goes to zero) even though the expected payout on an out-of-the-money put is a fraction of that.

- Capital utilisation is typically low.

Co-located Options and Perps, Offchain Matching (Aevo). Options and perpetuals share a cross-margin account, so market makers can hedge option inventory with perps on the same platform without routing to an external venue.

- However, Aevo’s matching engine and risk checks run offchain, with settlement posted to the chain.

- The exposure window between write and hedge shifts from a protocol infrastructure problem to a sequencer trust problem: the sequencer determines fill order, and the onchain settlement layer has no way to enforce that a hedge fill preceded the option mint.

Offchain Delta Hedging (Lyra, now Derive). Lyra v1 used an offchain keeper that read oracle prices, computed hedge adjustments, and sent separate transactions to external perp venues (GMX, Synthetix).

- Derive v2 moved to a CLOB where individual market makers manage their own delta.

- In both architectures, the option write and the hedge fill are separate operations: the options contracts are onchain, but the hedge is not guaranteed to fill before the option exists.

The Limitation: The Exposure Window

An automated onchain options vault has no discretion over when to hedge: any unhedged window is unmanaged risk. On every existing async venue, the initial hedge lands in a later block than the option write. The vault compensates by overcollateralizing, capping position sizes, or widening spreads, all of which reduce capital efficiency or competitiveness.

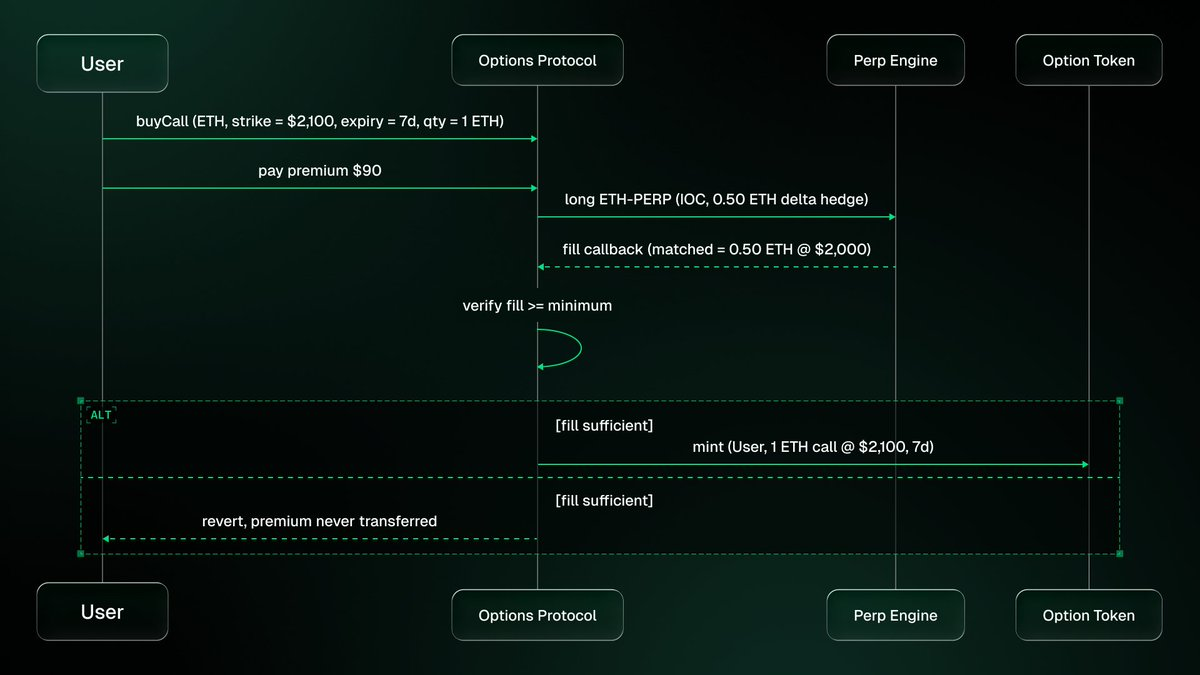

The strongest possible invariant is: the option is not minted unless the initial delta hedge is confirmed in the same transaction. No async venue can enforce this: the hedge transaction often lands in a later block.

With Atomic Composability

The hedge is established within the same transaction that writes the option.

Delta rebalancing is also atomic. As ETH price moves and delta changes, a keeper calls the rebalance function. The contract reads the current hedge size from onchain state, computes the new target delta, and adjusts the perp position (additional buy if delta increased, reduce-only sell if delta decreased) within the same transaction. The read and the adjustment are in the same transaction.

At expiry, the contract computes intrinsic value, pays the option holder, closes the hedge, and returns residual USDC, all in one transaction.

The product this enables is a fully onchain, self-hedging options market maker with provably delta-neutral books at all times, no offchain infrastructure, and Greeks auditable at any block height.

Alternative Approach: Eliminating the Hedge Entirely (Panoptic)

Panoptic sidesteps delta hedging entirely by redefining the option as a repositioned Uniswap v3 LP position: the hedge is implicit in the LP mechanics rather than explicitly maintained. This removes the infrastructure dependency.

The List Does Not Stop Here

The six spotlights are not exhaustive. Some secondary products build on MarketCore:

Funding Rate Swap. One party pays a fixed rate per epoch; the other receives whatever the RISEx accumulator recorded as realized funding. Pendle Boros (live August 2025) and IPOR Protocol (over $100M TVL) are the closest implementations, but both route the float reference through an oracle or custodian reporting what the matching engine computed.

Funding Rate Futures. The long profits if realized funding exceeds the agreed rate; the short profits if it compresses, mirroring CME’s Fed Funds Futures applied to perp carry. No trustless onchain version exists because settlement requires reading what the matching engine accumulated over an epoch. The PT leg of Pendle Boros is the closest instrument, but it has no short leg: a rate bear has no position.

Leveraged Tokens. A 3x ETH vault holds a 3x ETH-PERP and rebalances continuously as price drifts leverage off target. Binance leveraged tokens run this pattern offchain with a daily rebalancing window; the gap between price move and rebalance introduces path dependency that compounds against holders in volatile markets. On RISEx, the vault reads mark price and position size from onchain state and executes the correcting order in the same transaction.

Power Perpetuals. A power-2 perp tracks price-squared, giving the holder convexity: a 10% up move gains more than a 10% down move loses. On RISEx, the write and the initial delta hedge share the same mark price in the same block.

Conditional Order Execution. An order that carries its own precondition: execute a perp long only if the spot-perp basis exceeds a threshold, or place a stop-loss only if portfolio margin drops below a floor. The condition reads live MarketCore state at execution time; if it fails, the transaction reverts and no order is placed. On any async venue, the condition is checked offchain before submission and may be stale by the time the transaction lands.

The Composability Stack

Each primitive above is standalone. Their compounding effect is the platform argument.

The synthetic dollar uses the perp book for hedging, the spot book for ETH conversion, the oracle for mark price, and AutoYield for margin yield: four components of MarketCore, composed in a single mint transaction. The options protocol uses the perp book for delta hedging and the oracle for option pricing. The basis vault uses both books simultaneously. Each is a customer of MarketCore state.

This is what it means for a perp venue to be infrastructure rather than just an exchange. An exchange executes trades for end users. Infrastructure executes trades for protocols, which serve end users. MarketCore is a perp and spot orderbook in onchain state; the architecture is open to new market types on the same Solidity-in-EVM surface. Every protocol integrating adds liquidity and activity, which makes the next integration more valuable, which attracts the next protocol.

Conclusion

Every perp venue competes on fees, liquidity, and UX. These advantages are real. They are also fungible: fees can be matched, liquidity can be incentivized, UX can be cloned.

Architecture cannot. Every use case in this article shares one prerequisite: the perp orderbook and the program composing with it must run in the same EVM. A synthetic dollar that hedges atomically. Options that delta-hedge in the same block as the option write. Liquidations that convert collateral without a gap between observation and execution. None of these ask for special treatment from MarketCore. They ask only that MarketCore exists onchain and that Solidity can read its state.

That is the barrier. Async execution does not produce a degraded version of these products. It makes them structurally impossible without custodians, keepers, and reserve funds. Ethena’s Copper custodian, Lyra’s offchain keeper hedge, Binance’s daily rebalancing window: none of these are design preferences. Each is the only answer available when execution is async. On a synchronous venue, the problem they solve does not exist.

The exchange is the product. MarketCore is the infrastructure.RISEx is a fully onchain CLOB perp DEX built on RISE Chain. Read the previous articles in this series: